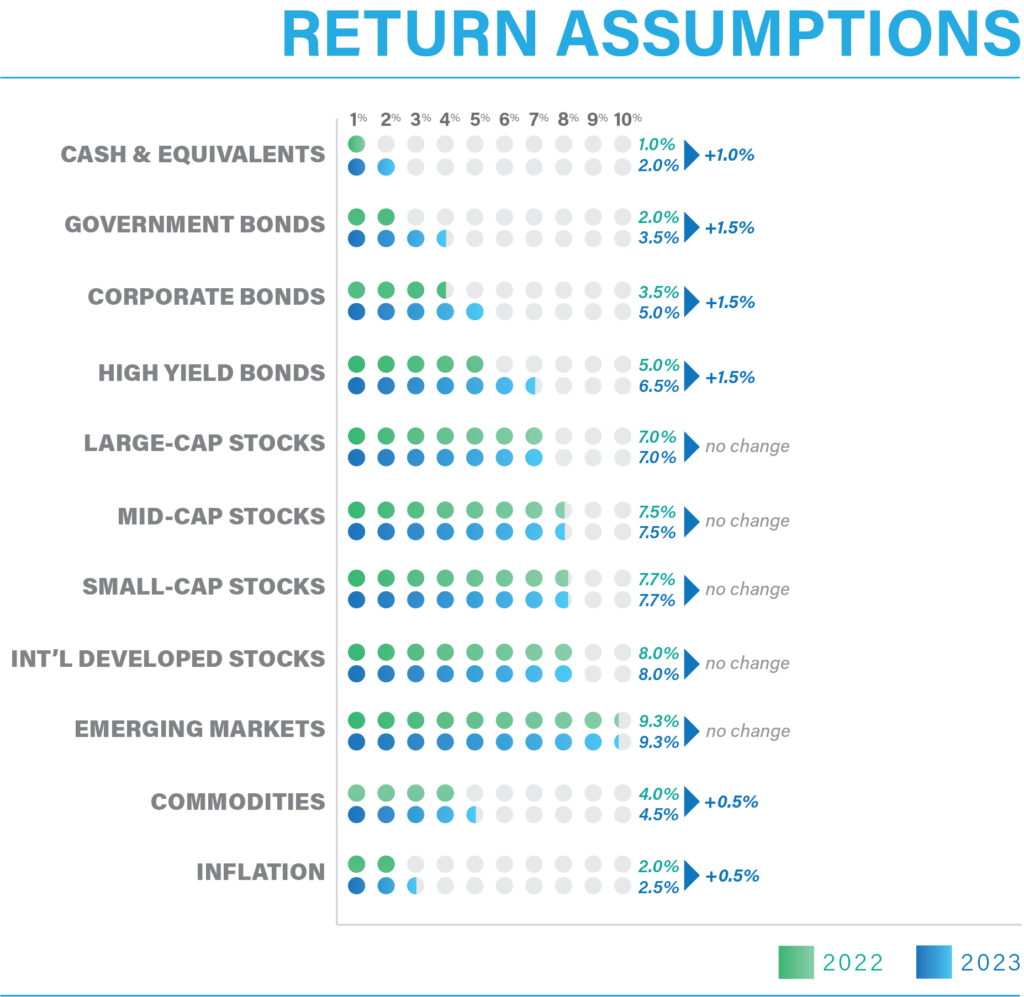

Black

Box

through which to view

the performance of the

2022 capital markets

Sometimes bad news isn’t as bad as it seems and can lead to good things ahead. This is the best lens through which to view the performance of the 2022 capital markets. With few exceptions, the major asset classes all fell in value last year despite the powerful rally in the middle of the fourth quarter. That’s the bad news.

2022 was a transition year. We have been living in a very unusual investing environment for the last fifteen years. Inflation has been well below the Fed’s 2% target, and interest rates fell to below even those paltry levels. This forced a lot of money away from relatively safe, fixed income investments towards equities, and in particular, stocks of companies with rapid growth. This caused earnings multiples to rise and while not readily visible, future return expectations to fall. Since this environment has continued for a long time, we’ve been fooled into thinking it is normal. A quick review of the history of capital markets would suggest, however, that the last fifteen years was the anomaly, not the norm.

This atypical environment ended in 2022 when the tremendous amount of stimulus needed to get us through the COVID pandemic caught up with the markets. Ultimately, more money was created than was probably needed. This excess cash met a global market that still hadn’t healed. With surging demand and constrained supply, inflation rapidly picked up. The war in the Ukraine exacerbated the situation, particularly in the energy and food markets. To combat inflation, the Fed jacked up interest rates over four percentage points in a short period of time causing turmoil in the capital markets.

At times like these, it is best to think of your investment portfolio as a black box which has one purpose: to generate income for your retirement needs. People focus on the principal shown as a solitary number on the cover of the black box. Unfortunately, this ignores the contents of the box: the investments that generate the returns which will satisfy your income needs throughout retirement. What’s in the box is almost as important as the number on the surface.

As a thought experiment, would you rather have a black box worth $100,000 earning 1.5% or one worth $88,000 earning 3.5%? The answer depends on your time horizon, and this not-so-made up example is exactly what happened in the US Treasury fixed income markets. If interest rates stabilize, you’ll recoup the $12,000 of lost principal in six years and will be better off every year thereafter. In fact, after 20 years investing at the higher 3.5% rate, you’ll have accumulated over $40,000 more than at the 1.5% rate. Short-term pain for long-term gain.

Another way to assess the value of a black box is to consider how much income it can generate. The first black box can only crank out $1,500 (1.5% of $100,000). The second black box cranks out $3,080 (3.5% of $88,000). So, while investors can accurately state that their fixed income portfolio fell 12% in 2022, they should also acknowledge their black box is stronger.

The other major component of these black boxes is your withdrawal rate. If the withdrawal rate is greater than the income the black box can earn, adjustments have to be made. Either investment options must change or the withdrawal rate needs to come down or the black box will fail. Figuring out these components is what we try to do with our financial planning software.

While inflation has been running much higher than 2.5%, we are trying to capture an average over the next 20 years for purposes of optimizing the black box. To get this estimate, we look at the market expectations for ten years which can be observed by comparing the yields on regular, nominal treasury bonds with inflation protected ones. Right now, that difference is 2.3%, but we believe there are structural issues that may keep it higher than market expectations.

To get the government bond, corporate bond, and high yield rates, we look at long-term yields and how they have trended over the past six months. The rates we’re using are pretty close to where the current 20-year yields are right now with the exception of high yield which is higher than the rate we’re using. This is because we also need to add in a default factor in those markets. As a recession is likely next year, default rates are sure to rise, making the realized yield lower than the stated yield.

Estimating stock rates are a bit trickier. There are more variables that go into an expected long-term rate of return for stocks than there are for fixed income. Some of the variables include current earnings versus the price of stocks relative to those earnings, the effects that inflation will play on earnings in the future, the growth rate of the economy, current risk-free interest rates, expected premiums to those interest rates, etc.

One of the better long-term predictors of returns is the cyclically adjusted price earnings ratio (CAPE). While not a very good tool for short-term swings, it does do pretty well at predicting 10-year returns. At present levels, and despite the decline in those multiples, the expected return from that model is very close to the 7% rate we have been using for quite a while now. So, we’re keeping our expectations the same as last year. International markets, and especially emerging markets have much lower CAPE ratios, and thus have higher expected long-term rates of return.

Finally, we boosted the expectations for commodities by 0.5%, in-line with our increased inflation expectations. While we feel the supply constraints we’ve faced since the pandemic began will dissipate with time, there are more troubling trends developing that seem to have more permanence. As one example, the trend towards re-shoring. We’ve enjoyed the benefits of a tightly integrated world for the last fifteen years which contributed to the very low inflation rates. This integration only works if the world is at peace. With Russia’s invasion of the Ukraine and China siding with Russia, that peace no longer exists. Companies are thus starting to move production back home which will be more expensive (though arguably more reliable).

May 2023 bring joy and peace to you and your family.

CFA® Chief Investment Officer